2026 Retirement Plan Compliance Deadlines and Important Dates

Retirement plan compliance in 2026 brings a full calendar of critical deadlines that employers cannot afford to miss. From new SECURE 2.0 requirements to annual filings, contribution cutoffs, and participant notice timelines, each date plays a role in keeping your plan aligned with IRS rules and supporting a smooth year of administration.

To make planning easier, we have organized the major deadlines that affect 401(k), 403(b), and Defined Benefit plans, along with the changes arriving on January 1, including Roth catch-ups for high earners and eligibility for long-term part-time employees. Use this guide to map out your year, stay ahead of filings, and maintain a compliant and efficient retirement plan.

Click the image below to download an excel spreadsheet of these dates.

2026 Retirement Plan Compliance Task Definitions

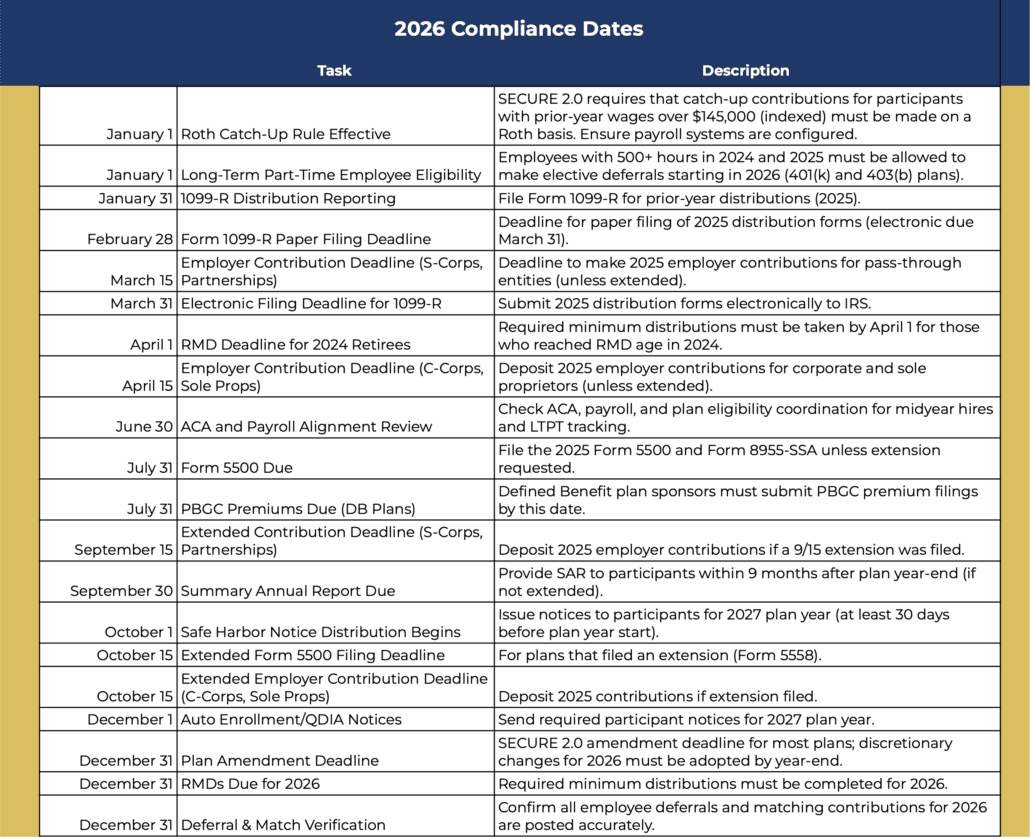

Roth Catch-Up Rule Effective (January 1)

The SECURE 2.0 requirement for high earners takes effect at the start of 2026. Participants with prior-year wages above $145,000 must make all catch-up contributions on a Roth basis. Employers should confirm payroll and recordkeeping systems can distinguish between traditional and Roth catch-up elections to prevent reporting issues.

Long-Term Part-Time Employee Eligibility (January 1)

Employees who worked at least 500 hours in both 2024 and 2025 must be allowed to make elective deferrals beginning in 2026. This applies to 401(k) and 403(b) plans and may require updates to your eligibility tracking. Employers should ensure their payroll and HR systems correctly flag LTPT employees.

Form 1099-R Distribution Reporting (January 31)

Form 1099-R must be issued to anyone who received a retirement plan distribution in the prior year. This includes rollovers, refunds, RMDs, and other taxable events. Timely reporting helps participants file accurate tax returns and avoids IRS penalties for late or incorrect forms.

Form 1099-R Paper Filing Deadline (February 28)

If you choose to file 1099-R forms on paper, they must be submitted to the IRS by February 28. Paper filing is less common due to the IRS preference for electronic submission, but the deadline still applies for those who use it. Keep in mind that electronic filings allow more processing flexibility.

Electronic Filing Deadline for 1099-R (March 31)

Plans filing electronically must submit all 1099-R forms by March 31. Electronic filing is now the standard for most organizations and reduces the risk of processing delays. Confirm your file format and submission system are aligned well before the due date.

Employer Contribution Deadline for Pass-Through Entities (March 15)

S-Corporations and partnerships must deposit prior-year employer contributions by March 15 unless they filed for a tax extension. These contributions may include matching, profit-sharing, or defined benefit funding. Meeting this deadline helps maintain deductibility for the prior tax year.

RMD Deadline for 2024 Retirees (April 1)

Individuals who reached their required beginning date in 2024 must take their first RMD by April 1, 2026. After this first distribution, all subsequent RMDs follow the normal year-end schedule. Employers should assist participants with reminders to avoid IRS penalties.

Employer Contribution Deadline for C-Corps and Sole Proprietors (April 15)

C-Corporations and sole proprietors must deposit prior-year employer contributions by April 15 unless they have an approved tax extension. Meeting this deadline allows the business to deduct the contribution for the prior tax year. Contribution types vary by plan design and funding requirements.

ACA and Payroll Alignment Review (June 30)

Midyear is an ideal time to review ACA compliance, payroll coding, and eligibility alignment. This includes verifying measurement periods, plan eligibility for part-time workers, and any changes affecting hours tracking. Conducting this review midyear prevents surprises at year-end.

Form 5500 Due (July 31)

For calendar-year plans, Form 5500 and Form 8955-SSA must be filed by July 31 unless an extension is requested. These filings provide the Department of Labor and IRS with a detailed review of plan operations and participation. Timely submission avoids penalties and keeps the plan in good standing.

PBGC Premiums Due for Defined Benefit Plans (July 31)

Defined Benefit plan sponsors must submit their PBGC premium filings by July 31. Premiums include flat-rate and potentially variable-rate amounts based on plan underfunding. Accurate reporting is essential to avoid penalties and ensure the plan remains compliant.

Extended Contribution Deadline for Pass-Through Entities (September 15)

If an S-Corp or partnership filed for an extension, employer contributions for the prior plan year are due September 15. This extended window allows additional time to calculate profit-sharing and other funding. Contributions made by this date remain deductible for the prior year.

Summary Annual Report Due (September 30)

Plans must deliver the Summary Annual Report to participants by September 30, assuming the Form 5500 was filed on time. The SAR provides a readable overview of plan financial activity and compliance. Timely distribution supports transparency and participant communication.

Safe Harbor Notice Distribution Begins (October 1)

Employers offering Safe Harbor 401(k) plans must begin sending participant notices by October 1 for the upcoming plan year. These notices describe employer contributions, rights, and plan features. Providing them on time is essential to maintaining Safe Harbor status.

Extended Form 5500 Filing Deadline (October 15)

For plans that filed Form 5558 for an extension, the final deadline to submit Form 5500 is October 15. This extended timeline supports more complex plans or those awaiting final audit results. Meeting the deadline ensures the plan stays compliant.

Extended Employer Contribution Deadline for C-Corps and Sole Props (October 15)

If an extension was filed, C-Corporations and sole proprietors must deposit their prior-year employer contributions by October 15. These contributions remain deductible for the prior tax year if deposited by this date. Many businesses use the extension window to finalize financials before funding.

Auto Enrollment and QDIA Notices (December 1)

Plans with auto enrollment or a Qualified Default Investment Alternative must distribute annual notices by December 1 for the next plan year. These notices explain default investment options and participant rights. Providing them early ensures participants have time to make informed choices.

Plan Amendment Deadline (December 31)

Most SECURE 2.0 and discretionary plan amendments for 2026 must be adopted by December 31. This includes compliance updates and optional enhancements chosen during the year. Plan sponsors should coordinate with their TPA and advisor to ensure all required amendments are documented.

RMDs Due for 2026 (December 31)

All required minimum distributions for 2026 must be completed by December 31. Timely distribution prevents participants from incurring significant IRS penalties. Employers should ensure systems and communication processes support accurate year-end tracking.

Deferral and Match Verification (December 31)

Before year-end closes, employers should confirm that all employee deferrals and matching contributions have been posted correctly. This includes reconciling payroll, plan records, and any corrections for missed or late deposits. Verifying totals now reduces operational issues during annual testing.