When business owners talk about their retirement plan, they often mention their advisor or the investment lineup. What rarely gets discussed is the role that quietly determines whether the plan actually works, stays compliant, and delivers the outcome the owner expects.

That role belongs to the Third Party Administrator, or TPA.

For businesses offering a 401(k), Safe Harbor plan, defined benefit plan, cash balance plan, or a combination of these, the TPA is responsible for the technical foundation of the plan. This is the work that happens behind the scenes, but it is also the work that keeps the plan from becoming a liability.

A strong retirement plan does not start with investments. It starts with sound design, careful administration, and ongoing compliance. That is where the TPA comes in.

The Role of a TPA in a Retirement Plan

A TPA is responsible for translating complex IRS and Department of Labor rules into a plan that actually functions inside your business.

This includes how the plan is structured, how contributions are calculated, how employees are treated under the rules, and how the plan adapts as the business grows or changes. In simpler plans, that work may feel invisible. In more complex plans, especially defined benefit or cash balance plans, it is essential.

Without experienced administration, even well-funded plans can fail required tests, trigger corrective contributions, or expose the owner to penalties they never expected.

Plan Design: Where Everything Starts

One of the most important things a TPA does happens before the plan is ever implemented.

Plan design determines whether a retirement plan supports the owner’s goals or works against them. This is where decisions are made about the type of plan, how contributions flow, and how benefits are allocated between owners and employees.

For highly compensated owners, design matters even more. Traditional 401(k) limits are often not enough, and defined benefit or cash balance plans can dramatically increase tax-deferred savings when structured properly. At the same time, those plans must meet coverage and non-discrimination rules, which is where experience becomes critical.

Good plan design anticipates growth, hiring, compensation changes, and even ownership transitions. Poor design reacts after the fact.

Ongoing Administration: Keeping the Plan Running Smoothly

Once a plan is established, the TPA manages the day-to-day and year-to-year administration that keeps everything on track.

For 401(k) and Safe Harbor plans, this includes monitoring eligibility, tracking contributions, confirming employer matches are correct, and ensuring Safe Harbor requirements are met each year. When laws change or the business evolves, the TPA manages plan amendments so nothing falls out of compliance.

Defined benefit and cash balance plans add another layer. Annual contribution calculations, coordination with actuaries, funding requirements, and ongoing monitoring all fall under the TPA’s oversight. When income fluctuates or staffing changes, the plan must be adjusted thoughtfully, not reactively.

In combination DB and DC plans, the TPA ensures the plans work together as a coordinated strategy rather than two disconnected benefits.

Compliance Testing and Why It Matters

Compliance testing is one of the areas business owners rarely see, but it is one of the most important.

Retirement plans are required to pass a series of annual tests designed to ensure fairness and compliance with federal regulations. These tests determine whether the plan disproportionately favors owners or highly compensated employees and whether enough employees are benefiting under the rules.

When a plan fails a test, it does not mean the plan is broken. It means corrections must be made, and those corrections can be costly if they are not identified early. A TPA’s role is to run these tests, interpret the results, and guide corrective action before small issues become expensive ones.

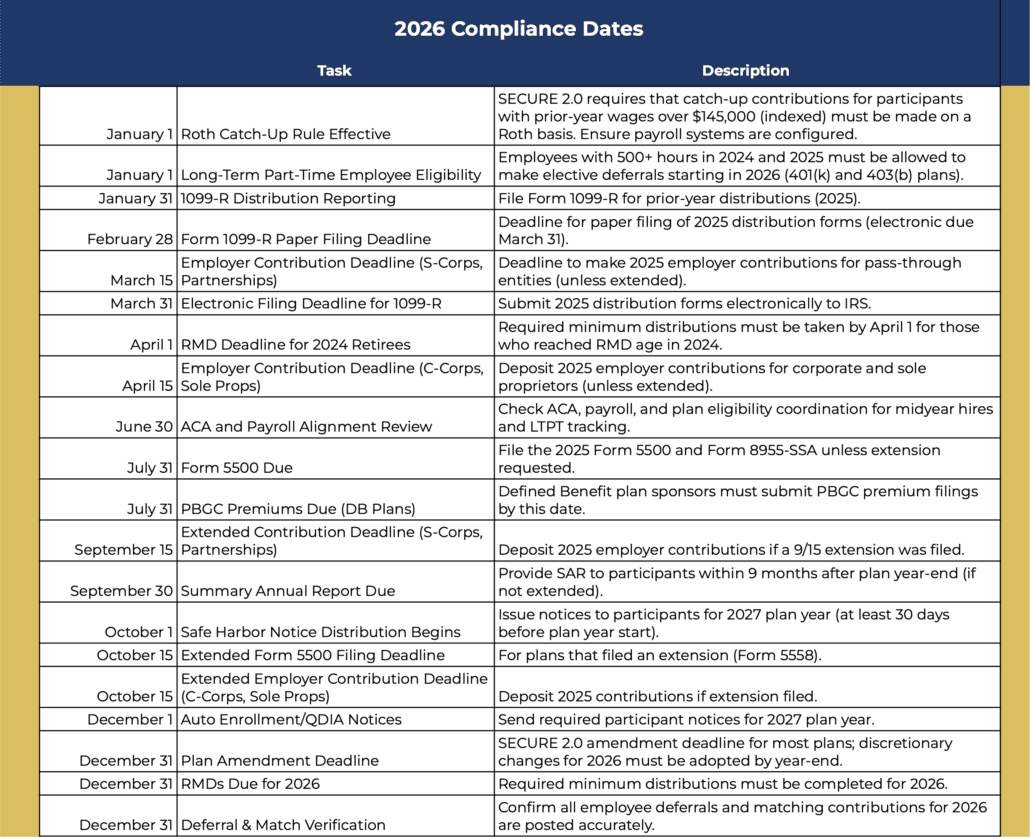

Filings, Forms, and Government Reporting

Every qualified retirement plan comes with reporting obligations. These filings are not optional, and errors can result in penalties or audits.

TPAs prepare and manage these filings on behalf of the plan sponsor. This includes Form 5500, actuarial schedules for defined benefit and cash balance plans, participant disclosures, and required plan updates. If a question arises from the IRS or Department of Labor, the TPA provides documentation and support.

For business owners, this removes a significant administrative burden and reduces the risk that something is missed or filed incorrectly.

Fiduciary Responsibility: What the Owner Still Owns

Hiring a TPA does not eliminate fiduciary responsibility. Business owners remain responsible for selecting and monitoring service providers and ensuring the plan operates in the best interest of participants.

What a strong TPA does is reduce fiduciary risk. By keeping the plan compliant, flagging issues early, and ensuring the plan is administered correctly, the TPA acts as a safeguard. Problems are identified before they escalate, and decisions are made with full visibility into the regulatory impact.

What a TPA Takes Off Your Plate

For most business owners, especially those running lean operations, the value of a TPA is not just technical expertise. It is peace of mind.

A good TPA removes the need to interpret regulations, track testing deadlines, prepare filings, or coordinate between multiple service providers. Instead of reacting to compliance issues, the owner gains a plan that runs smoothly and predictably.

That clarity allows owners to focus on running their business while knowing their retirement plan is doing what it was designed to do.

Why the Right TPA Matters

Not all TPAs operate the same way. Experience matters, especially for closely held businesses and highly compensated owners.

The right TPA understands how to balance owner objectives with employee benefits, without overcomplicating the plan or creating unnecessary risk. They think long-term, not just about passing this year’s tests, but about how the plan will function five or ten years down the road.

At Mirador, retirement plans are treated as long-term strategies, not off-the-shelf solutions. Each plan is designed intentionally, administered carefully, and supported with the level of attention business owners expect when the stakes are high.

A well-designed plan does more than satisfy compliance requirements. It becomes a meaningful tool for tax efficiency, employee retention, and long-term financial security, for both owners and the people who help build the business.